As anyone paying any attention to financial markets in recent times can tell you, interest rates have been rising. After hitting their long-term lows in 2016, Australia government bond (as well as the US) yields have been trending higher. There are a range of drivers for this but some of the key ones include rising inflation expectations, growing budget deficits, expectations for reduced central bank purchases and increased supply.

It’s reasonable to assume that you might want to avoid investing is bonds in this environment if you are familiar with the concept of duration. Bonds are often issued as “fixed rate”, meaning the regular interest payment (called the “coupon”) is agreed and fixed on day one. If yields generally available in the market increase after a particular bond is issued, the price of bonds issued recently will then need to move lower to reflect the new fair market pricing. Imagine you paid $100 yesterday for a 3% per annum income stream. Today, the market will offer you a 3.2% annual income stream from the same borrower, for the same price. The 3% income stream doesn’t look like the best deal anymore. As you can see, there is an inverse relationship between bond prices and yields. (The breakout box below gives more detail on the duration concept.) In summary, investors are likely to suffer short-term capital losses from bonds as interest rates rise, and longer duration bonds will suffer more.

So how do investors avoid the risk of higher interest rates?

One way is to avoid fixed-rate bonds.

Not all bonds are issued with fixed coupons. Some bonds are “floating rate”, meaning the coupon paid changes as underlying interest rates change. This type of security helps to mitigate the risk associated with rising interest rates. As rates move higher, the coupon is adjusted higher as well mitigating the need for the price of the security to move lower to reflect the fair value of the higher interest rate environment.

The other alternative is to simply close your eyes and ignore the volatility.

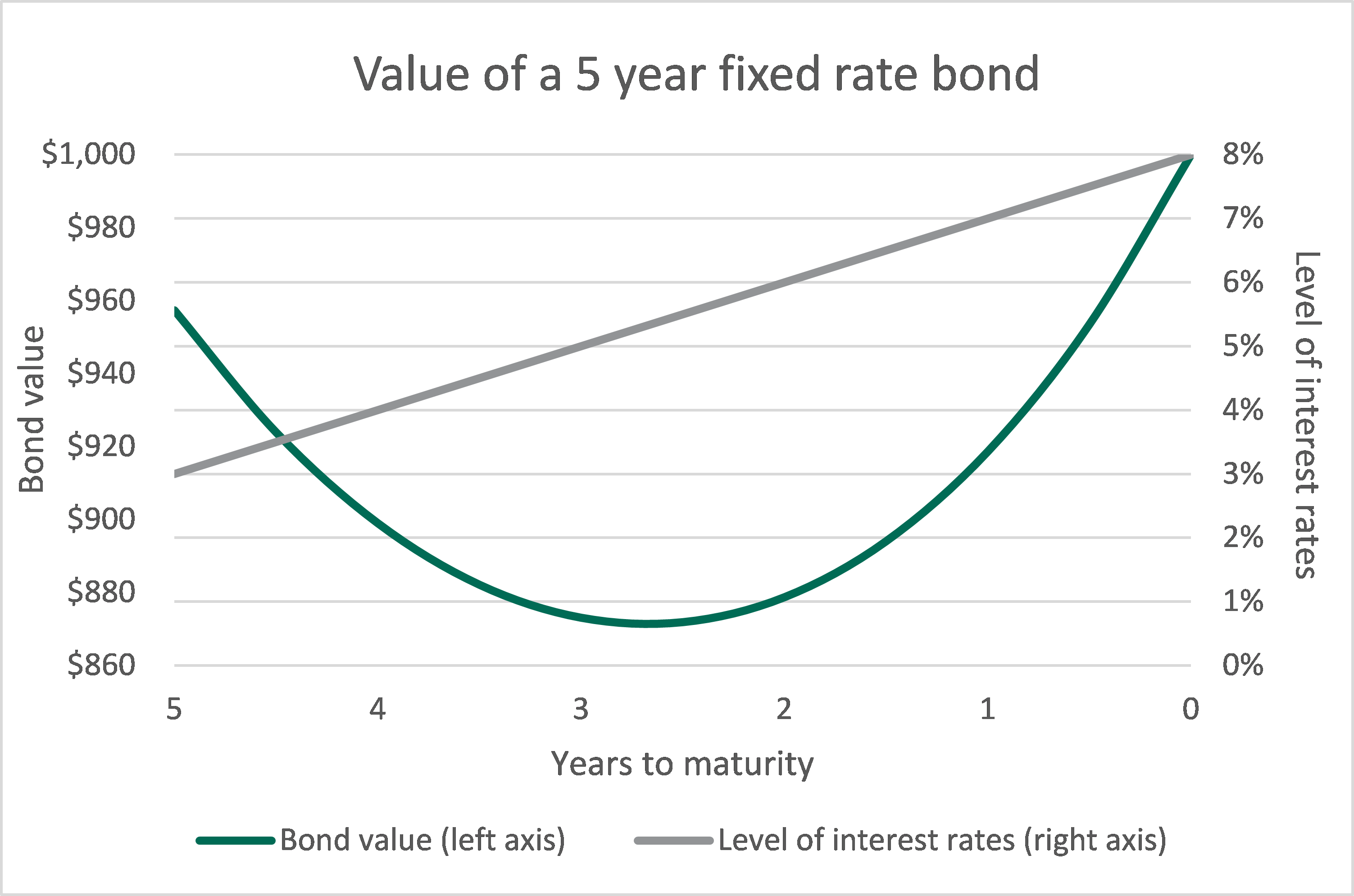

As the chart above shows, as long as the bond issuer doesn’t default, you will eventually get all your coupon and capital back at maturity. This approach might work fine if you can “set and forget” your portfolio. However, many people who invest in fixed income view the asset as the defensive part of their portfolio and might not choose to do this. If you own a bond or fund with an interest rate duration of five years and interest rates rise by 2%, the security/fund would be down by roughly 10%. In our view, this doesn’t seem like a favourable outcome for what is expected to be the defensive allocation in your portfolio.

For an actively managed fixed income fund, it’s quite straightforward to buy floating rate securities. Professional investors can also buy fixed rate bonds and hedge out the interest risk. Although, for individual investors buying bonds or funds with significant embedded interest rate risk and then too hedging this out, may be more of a challenge.

In our opinion, with interest rates likely to rise further, it may be worth investors considering a low duration fund. Otherwise, you might like to ensure you buckle up for what may be a wild ride in the coming years.

This is the opinion of the author, Mark Mitchell, Portfolio Manager.

Anything that increases the average time that an investor has to wait before receiving all coupon and principal payments increases the sensitivity of a bond to interest rates. This interest rate sensitivity is called duration, and it is measured in years. The following factors lengthen the duration of a bond, all else being equal:

- Longer time until maturity and return of principal;

- A lower coupon payment (as a proportion of principal);

- Market yields – as yields fall (and the price of a bond increases), its duration will also increase.

It is particularly interesting to note that with interest rates at very low levels, two things have happened:

- (i) the probability of interest rates moving higher over time is increased; and

- (ii) the potential negative price impact of a given move to higher interest rates is also increased, because low interest rates themselves increase duration.