Nicki Bourlioufas – Morningstar

Australian government bond yields have dropped to record lows in recent times amid fears of a local and global economic slowdown, with investors flocking to the safety of bonds as a buffer to expected ongoing volatility.

The Australian 10-year bond yield has sunk to historical low levels at about 1.68 per cent as at 20 May 2019, while short-end government yields have also fallen on expectations that the Reserve Bank of Australia may cut interest rates twice this year.

Prices, which move opposite to yields, have risen sharply as demand for bonds has jumped amid high huge swings in stock markets fuelled by trade tensions between the US and China, raising fears of a global and local recession.

Stephen Miller, investment strategist with fund manager GSFM, says the rally in government bonds was initially prompted by the large downdraft in equity markets in late 2018, and has continued since then, as investors flock to more secure government bonds.

“Despite the recovery in equity markets in the first few months of 2019, bond yields drifted even lower as the US Federal Reserve indicated that previous plans to raise [interest rates] were now in abeyance and financial markets began to price the prospect of the US Fed reducing the policy rate later in 2019,” says Miller.

“The experience of the last 20 years or so suggests that government bonds generally perform well during market corrections (or ‘risk-off’ episodes). In other words, bond and equity returns have tended to exhibit negative correlation,” he says.

However, “with bond yields already low, however, the extent of that negative correlation may decline,” says Miller.

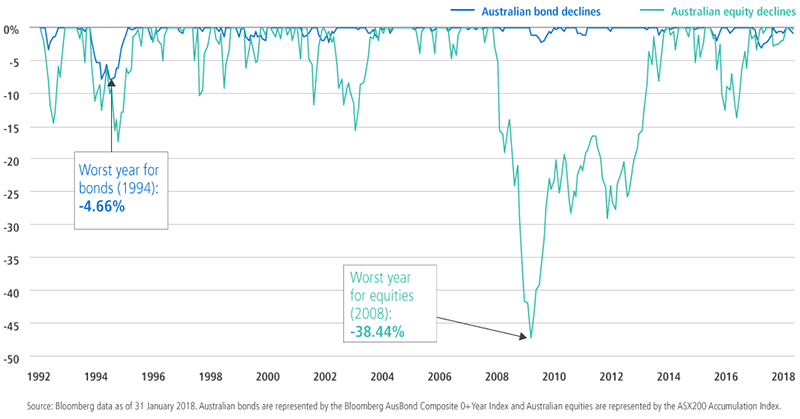

The chart below from global bond fund manager PIMCO shows that historically, Australian bond market declines have been much less severe than the stock market.

Corporate bonds have rallied too in recent times with the rebound in equity markets. The Bloomberg AusBond Composite 0+ Index is up about 9.01 per cent over the year, compared to 6.1 per cent for the S&P/ASX 200 Index as at 20 May.

“Most corporate bonds have rallied along with government bonds. The longer that interest rates remain low and stable, the better the chances that credit spreads continue to tighten,” says Brad Dunn, senior credit analyst at Daintree Capital.

Dunn says bonds are designed to provide income over time. Therefore, they provide a useful balance to growth assets such as equities.

“Ultimately, a strong case can be made for having some exposure to bonds over most phases of the investment life cycle,” says Dunn.

“For investors that are more focused on capital growth with a long investment horizon, perhaps a higher equity exposure would make sense. Investors who have shorter investment horizons or value capital preservation might consider a higher fixed income allocation.”

Bond funds offer income, diversification opportunity

According to Daintree’s Dunn, the key factor when choosing a bond fund is determining whether the characteristics align with your investment goals.

“For example, if you require a higher level of income, then perhaps lower-yielding government bonds may be unsuitable to achieve that objective. Similarly, if you are seeking to minimise volatility, a fund with high duration (exposure to changes in interest rates) may not meet expectations despite the high credit quality of the fund holdings.”

Having some exposure to corporate bonds may also make sense as it allows investors to diversify risk across dozens, or even hundreds of issuers, minimising the damage that a default could have on portfolio performance.

GSFM’s Miller says that in an environment where bond yields are extraordinarily low, an “absolute return” or “unconstrained” bond fund investment can act as a complement to traditional bond portfolios benchmarked to a conventional index.

“‘Absolute return’ or ‘unconstrained’ portfolios have the conservative return profiles that one requires of defensive portfolios but typically have less duration exposure than conventional bond portfolios benchmarked to an index,” says Miller.

“This means that they will generally outperform conventional indices in a rising bond yield environment (not an unimportant consideration in an era of extraordinarily low bond yields).

“They typically will also seek more diversified sources of return such as exposures to other fixed income sectors such as inflation-linked bonds, corporates, high yield, emerging markets, foreign exchange, asset backed securities etc,” Miller says.

Dunn adds that it is important to understand whether the fund is linked to a benchmark, which forces it to own certain bonds and maintain a certain duration, or whether the fund manager has some flexibility to invest with a degree of judgment to achieve the best risk-adjusted returns.