In these times where every basis point counts, hybrids stand tall, offering the highest yields for an investment grade credit rating. As a reminder, a credit rating is simply an opinion of the likelihood that a bond will default during its time on issue.

While hybrids are attractive on a gross yield or spread basis, there is no such thing as a free lunch. These higher relative returns come with a catch – complexity.

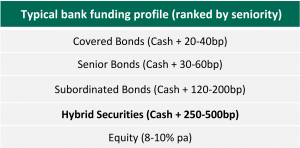

The liability side of a bank balance sheet is multi-layered, ranging from super-senior instruments and customer deposits that are highly protected at the top of the stack, through to hybrid securities that sit just above shareholders equity. The compensation on offer to securities at each level generally reflects their seniority, but can be influenced by any number of other factors.

Table 1: Bank funding profile

Source: Daintree estimates

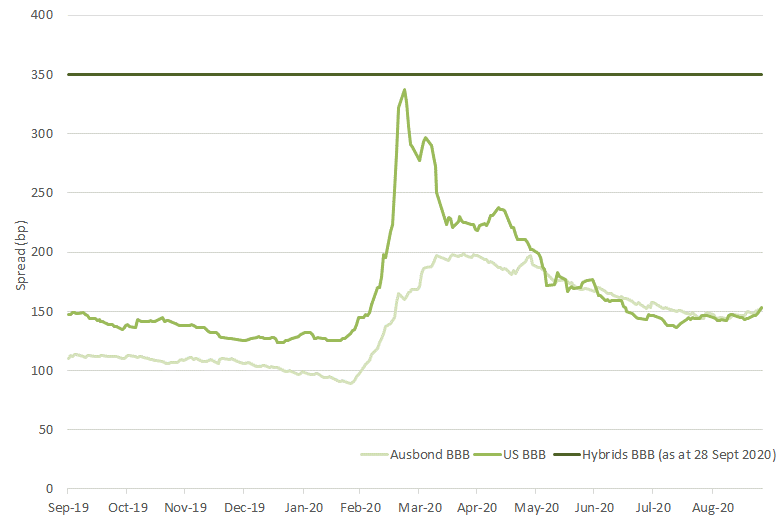

The real attractiveness starts to show through when you compare hybrid yields to corporate bonds with the same credit ratings. We compare hybrid spreads to two indices of BBB-rated corporate bonds, one Australian and one American. We have set the hybrid curve to current spreads, inclusive of franking credits where available.

Figure 1: BBB spreads

Source: Bloomberg

The chart shows a clear spread advantage to hybrids with a BBB rating. Even in the turmoil of COVID-19 where credit spreads widened quickly and dramatically, the US BBB index did not reach the spread levels that Australian hybrids have subsequently reverted to. For context, Australian hybrid spreads widened to as high as 700bps over cash for a short period as liquidity dried up.

Daintree has been doing a lot of work understanding the preparedness of the banking sector to navigate and facilitate a strong recovery. Our research gives us comfort that banks held in Daintree portfolios are beneficiaries of the work undertaken in years past to build capital buffers and maintain high lending standards.

However, challenges remain. With inevitable loan losses likely to materialise progressively over coming years, capital will need to be maintained. Consequently, the prospect of dividends from banks globally has fallen. Australian banks are effectively limited to paying up to 50% of profits in dividends, whereas in years prior they have paid out as much as 85% of profits.

Conclusion

While yield remains an important factor for many investors, hybrids will always look attractive when compared to similarly rated alternatives. The many banks that issue these securities have a pivotal part to play in the economic recovery, but they will still have to make many tough decisions impacting customers and shareholders. Therefore, we believe hybrids hold a unique place in the corporate credit space with a balance between yield and quality for investors with the appropriate risk tolerance and investment horizon.

Disclaimer: Please note that these are the views of the writer and not necessarily the views of Daintree Capital. This article does not take into account your investment objectives, particular needs or financial situation.